Introduction: Decoding Interest Rate Cycles in the United States

Interest rate cycles drive the pulse of the global economy, with their effects hitting hardest in the United States. These shifts in borrowing costs, largely steered by the Federal Reserve, shape everything from home loan affordability to the bottom lines of major businesses. For U.S. investors and traders, grasping these patterns goes beyond theory-it’s a must for smart moves in the markets. Heading into 2025, getting a read on upcoming rate changes and their reach across sectors is key to staying ahead. This guide breaks it all down, giving you the insights to handle the twists and turns of American monetary policy.

What Are Interest Rate Cycles and Why Do They Matter for the US Economy?

In the U.S., interest rate cycles track the ups and downs of the central bank’s key rates, moving from hikes that tighten policy to cuts that loosen it. The Federal Reserve, or the Fed as it’s commonly known, sets the federal funds rate, which applies to short-term loans between banks but sets the tone for everything else-from personal loans and home mortgages to business financing.

The Fed uses these rates to hit its two main goals: keeping unemployment low while holding inflation steady around 2%. In booming times with rising prices, it bumps rates up to temper growth and prevent overheating. When things cool off or tip into recession, it drops them to spark lending, business expansion, and household spending. These swings touch every corner of the economy, serving as a vital sign of its strength and trajectory.

The Four Stages of a US Interest Rate Cycle

Breaking down the phases of these cycles helps investors and traders spot opportunities and tweak their approaches. Though each cycle has its quirks, they tend to unfold in a familiar sequence.

Expansion (Low Rates)

This phase kicks in after a dip or downturn, with the Fed holding rates low-often close to zero-to jump-start activity. Borrowing gets cheap, fueling everything from home buys to factory upgrades.

- Key Features: Robust hiring, upbeat consumer outlays, climbing company earnings, and usually a climbing stock market. Prices stay tame at first but can edge higher later on.

- Watch For: Unemployment dipping low, GDP on the rise, and CPI ticking up but not yet out of the Fed’s comfort zone.

- Fed Approach: Easy money policies to boost jobs and growth.

Peak (Rising Rates)

Once growth picks up steam and prices start climbing faster, the Fed steps in with rate increases to keep things from boiling over. Policy shifts from supportive to restrictive.

- Key Features: Solid expansion persists, but inflation sticks around. Markets can get choppy as higher costs hit investments.

- Overheating Signals: Wages surging, raw material costs jumping, bubbles in stocks or housing, and inflation past the 2% mark.

- Fed Moves: The FOMC rolls out hikes to rein in spending and tame prices.

Contraction (High Rates)

Rates top out after a string of increases and stay there, curbing inflation at the risk of slowing the economy-possibly into a slump.

- Key Features: Growth fades, earnings stall, jobs soften, and prices ease off. Debt stays pricey, though.

- Recession Risk: Elevated rates squeeze spending and investment, cutting overall output.

- Fed Stance: It keeps rates firm until inflation trends down steadily and the job market cools.

Trough (Falling Rates)

With slowdown clear and prices in check, the Fed starts slashing rates to aid a rebound. Cheaper credit aims to revive investment and spending.

- Key Features: Economy contracts or stalls, inflation drops, and unemployment climbs. Traders often price in cuts early.

- Slowdown Signs: GDP weakens, companies cut back, and hiring slows.

- Fed Action: Cuts flood the system with cash to prop up activity.

The Federal Reserve’s Role in Shaping US Interest Rate Cycles

At the heart of U.S. monetary policy sits the Federal Reserve, whose choices directly mold these cycles. Knowing how it works and what tools it wields is essential for anyone trading or investing in American markets.

Mandate and Tools

Congress gave the Fed a dual mission: promote full employment and steady prices. It pursues this through a toolkit that includes:

- Federal Funds Rate: The core rate for bank-to-bank loans, which echoes across all borrowing.

- Quantitative Easing (QE) and Tightening (QT): Buying bonds (QE) to flood markets with money or selling them (QT) to pull it back, affecting longer-term rates.

- Reserve Requirements: Rules on how much cash banks must keep on hand, used sparingly these days.

- Discount Window: Emergency loans to banks at a set rate.

FOMC Decisions

The FOMC, made up of 12 voting members, convenes roughly eight times yearly to review data and decide on rates or other steps. Global markets hang on their words, especially lately as they’ve hiked to fight sticky inflation.

Communication and Forward Guidance

The Fed’s words carry as much weight as its deeds. Press releases, talks from officials, and tools like the dot plot-showing members’ rate forecasts-guide expectations. This forward guidance steadies nerves and shapes bets before votes even happen.

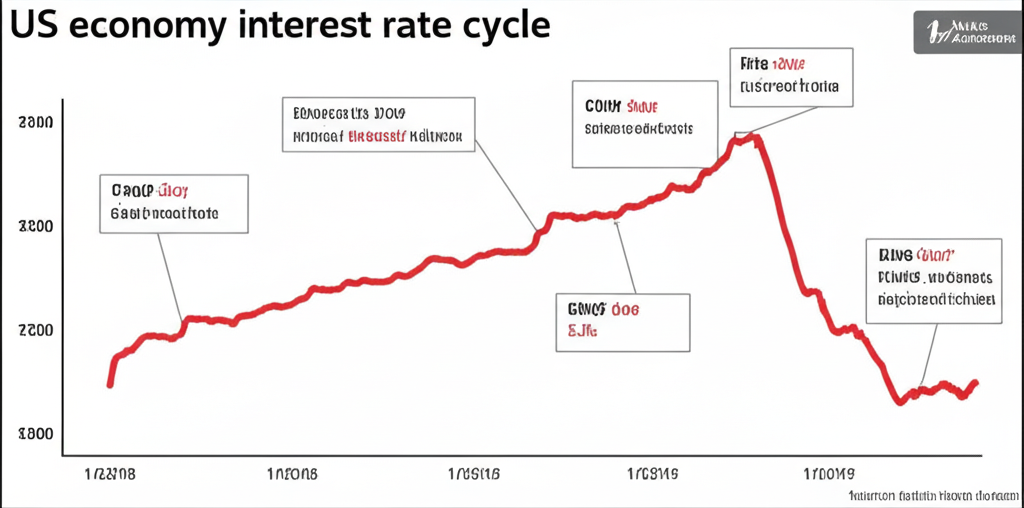

A Historical Perspective: US Interest Rate Cycles Through the Decades

Looking back reveals how the Fed has tackled crises and booms, offering clues for today’s moves.

The 1970s brought double-digit inflation, prompting Fed Chair Paul Volcker to jack rates to almost 20% by 1981, accepting a recession to crush price spikes and restore calm.

The 2008 crash flipped the script: rates plunged to zero, paired with massive QE to thaw credit and spark recovery, proving the Fed’s readiness for bold, nontraditional steps.

Then came COVID-19 in 2020, with rates slashed again and QE ramped up, only for hikes to follow in 2022 as prices soared. These swings show how policy bends to fit the moment.

Check the Federal Reserve’s site for a Fed funds rate history chart, which maps out these highs and lows, from the Volcker era’s peaks to the long stretches of near-zero rates. Past patterns shed light on what might come next.

Impact of US Interest Rate Cycles on Key Sectors and Investments in 2025

Rate cycles send shockwaves through the economy and markets, and for 2025, spotting these effects will shape smart plays.

Bonds and Fixed Income

Bond prices move opposite to rates: hikes make new bonds pay more, dropping the value of old ones with lower yields. U.S. Treasuries set the pace for other debt, so rising rates boost new-issue returns but hit current holders with losses.

Equities and Stock Market

Stocks react in layers. Higher rates hike company debt costs, crimping profits and growth-especially for tech-heavy growth names, whose future cash flows get discounted harder. Value plays hold up better, and banks often gain from wider margins, while debt-laden areas like real estate feel the squeeze.

Real Estate and Mortgages

Mortgage rates track Fed moves closely, making homes pricier to finance and cooling buyer interest, which can stall or drop prices. Rate drops do the reverse, igniting demand. In 2025, mortgage trends will signal the housing sector’s vitality.

Consumer Spending and Loans

Higher rates jack up costs on cards, car loans, and more, curbing big-ticket buys and denting confidence-a drag on GDP. Cuts flip this, freeing up cash for spending.

The US Dollar and Forex Market

Rate gaps move currencies: Fed hikes draw foreign cash chasing better yields, strengthening the dollar and boosting inflows. This powers carry trades, borrowing cheap abroad to buy USD assets. Forex players must track Fed signals for 2025 to gauge pairs like EUR/USD.

Navigating Interest Rate Cycles in the United States: Strategies for Investors and Traders in 2025

Tuning strategies to the rate environment sets up success in 2025’s markets.

Portfolio Adjustments

- Sector Rotation: In hike phases, shift from tech growth stocks to steadier value ones in finance, manufacturing, or health care.

- Dividend Stocks: Reliable payers provide yield buffers in shaky times.

- Alternative Investments: Mix in REITs, commodities, or private equity for balance beyond stocks and bonds.

Forex Trading Strategies

- Carry Trades: With U.S. rates outpacing others, go long USD versus low-yield currencies-but watch for FX swings.

- Trend Following: Eye Fed news and data for directional cues in USD pairs.

- Understanding Fed Announcements: FOMC releases, Chair Powell’s talks, and projections spark big moves-be ready.

Hedging Against Rate Volatility

Tools like rate futures, options, or swaps let you protect against surprises. Betting on hikes? Short bond futures to counter bond portfolio dips.

Long-Term Planning

Diversify always, and revisit your mix to match goals and risk levels, no matter the cycle.

Forex Brokers and Interest Rate Cycles: Key Tools and Features

The right forex broker amps up your edge in rate-driven trades, with tight spreads, leverage, and data tools to track Fed impacts.

Top International Brokers for Advanced Trading Strategies During Rate Cycles

For rate-fueled strategies, pick brokers with strong setups. U.S. folks, stick to CFTC/NFA-regulated options.

- Moneta Markets: A solid pick for global traders riding rate waves, Moneta Markets holds an FCA license and delivers tight spreads on forex, commodities, indices, and cryptos-perfect for capturing currency shifts. It supports MT4, MT5, and a user-friendly WebTrader with pro charting for volatile sessions. Plus, top-notch education and support help refine rate-based plays. Note: Moneta Markets doesn’t serve U.S. clients. Americans, choose CFTC/NFA-regulated brokers.

- OANDA: Known for slim spreads and platforms like fxTrade and MT4, OANDA shines with real-time news, calendars, and analysis for Fed-focused trading. It’s CFTC/NFA-regulated in the U.S., ensuring safety.

- IG: With broad markets from forex to commodities, IG offers sharp pricing, advanced charts, and learning resources. Regulated across top spots, its U.S. side focuses on futures but global tools aid rate cycle trades.

The 2025 Outlook for US Interest Rates: What to Expect

Predicting rates involves guesswork, but current trends and Fed hints point to paths ahead.

Current Economic Climate

By late 2024, the U.S. economy holds firm, but jobs data, growth figures, and price pressures guide the Fed’s hand toward its 2% inflation goal without sparking unemployment spikes.

Fed Projections and Market Expectations

The dot plot reveals FOMC views on future rates, while futures markets bet on changes. Both evolve with fresh stats.

Potential Scenarios for 2025

- Continued Tightening (Less Likely): Stubborn inflation could mean more hikes or holds, pressuring growth.

- Plateau/Holding Pattern (Likely): Rates stay high if prices ease gradually and jobs stay strong-a “higher for longer” vibe.

- Easing (More Likely if Data Weakens): Clear slowdowns or recession would trigger cuts, lifting stocks but flagging trouble.

Experts see 2025 with steady or easing rates, all hinging on the numbers.

Conclusion: Adapting to Evolving US Interest Rate Cycles in 2025

Rate cycles define U.S. finance, swaying returns, spending, and the dollar’s clout. Into 2025, track Fed moves and indicators closely-it’s table stakes. Adjust portfolios wisely and leverage forex tools from brokers like OANDA or IG to ride the waves and come out stronger.

Frequently Asked Questions (FAQ)

What are interest rate cycles?

Interest rate cycles refer to the recurrent pattern of rising and falling benchmark interest rates, primarily influenced by a central bank (like the Federal Reserve in the United States). These cycles are driven by economic conditions such as inflation, employment, and economic growth, impacting borrowing costs and investment decisions across the economy.

Is the Fed going to lower interest rates in 2025?

The likelihood of the Federal Reserve lowering interest rates in 2025 depends heavily on incoming economic data, particularly inflation trends and labor market conditions. While market expectations often lean towards some easing, the Fed has indicated it will remain data-dependent. A significant slowdown in the US economy or a sustained drop in inflation towards the 2% target would increase the probability of rate cuts.

Will interest rates ever go back down to 3% again?

While historical data shows periods of very low interest rates, whether the federal funds rate will return to 3% again is uncertain. The Federal Reserve’s long-term projections and the current economic paradigm suggest that future low rates might not be as extreme as those seen post-2008 or during the pandemic, but economic circumstances can change. Factors like global growth, inflation targets, and potential future crises could influence this.

What date is the next interest rate decision in the United States?

The Federal Open Market Committee (FOMC) meets eight times a year to discuss and vote on interest rate decisions. The specific dates for these meetings are publicly available on the official Federal Reserve website. Investors and traders should consult the Fed’s calendar for the exact dates of upcoming announcements, as these often trigger significant market movements.

How do interest rate cycles affect the US dollar?

Interest rate cycles significantly impact the US dollar. When the Federal Reserve raises interest rates, it generally makes dollar-denominated assets more attractive to international investors due to higher returns, leading to increased demand for the USD and its appreciation. Conversely, falling US interest rates can weaken the dollar as capital seeks higher yields elsewhere. This dynamic is crucial for forex traders.

What is the Fed interest rates chart history for the United States?

The Federal Reserve provides extensive historical data on the federal funds rate, which can be found on its official website. This chart history shows periods of significant rate hikes (e.g., the early 1980s to combat inflation) and prolonged periods of low rates (e.g., post-2008 financial crisis and during the COVID-19 pandemic). Analyzing this history helps in understanding the Fed’s past responses to economic conditions in the United States.

How can a forex broker like Moneta Markets help me trade during US interest rate cycles?

A broker like Moneta Markets can be highly beneficial for trading during US interest rate cycles by offering competitive spreads and robust platforms (MT4/MT5, WebTrader) crucial for executing strategies based on rate differentials. Their diverse asset offerings allow traders to capitalize on various currency pair movements influenced by Fed policy. Moneta Markets provides essential analytical tools and educational resources, helping traders understand market dynamics and make informed decisions, especially for international traders looking to leverage interest rate shifts. (Note: Moneta Markets does not accept US clients; US residents must use locally regulated brokers like OANDA or IG for their specific products.)

No responses yet